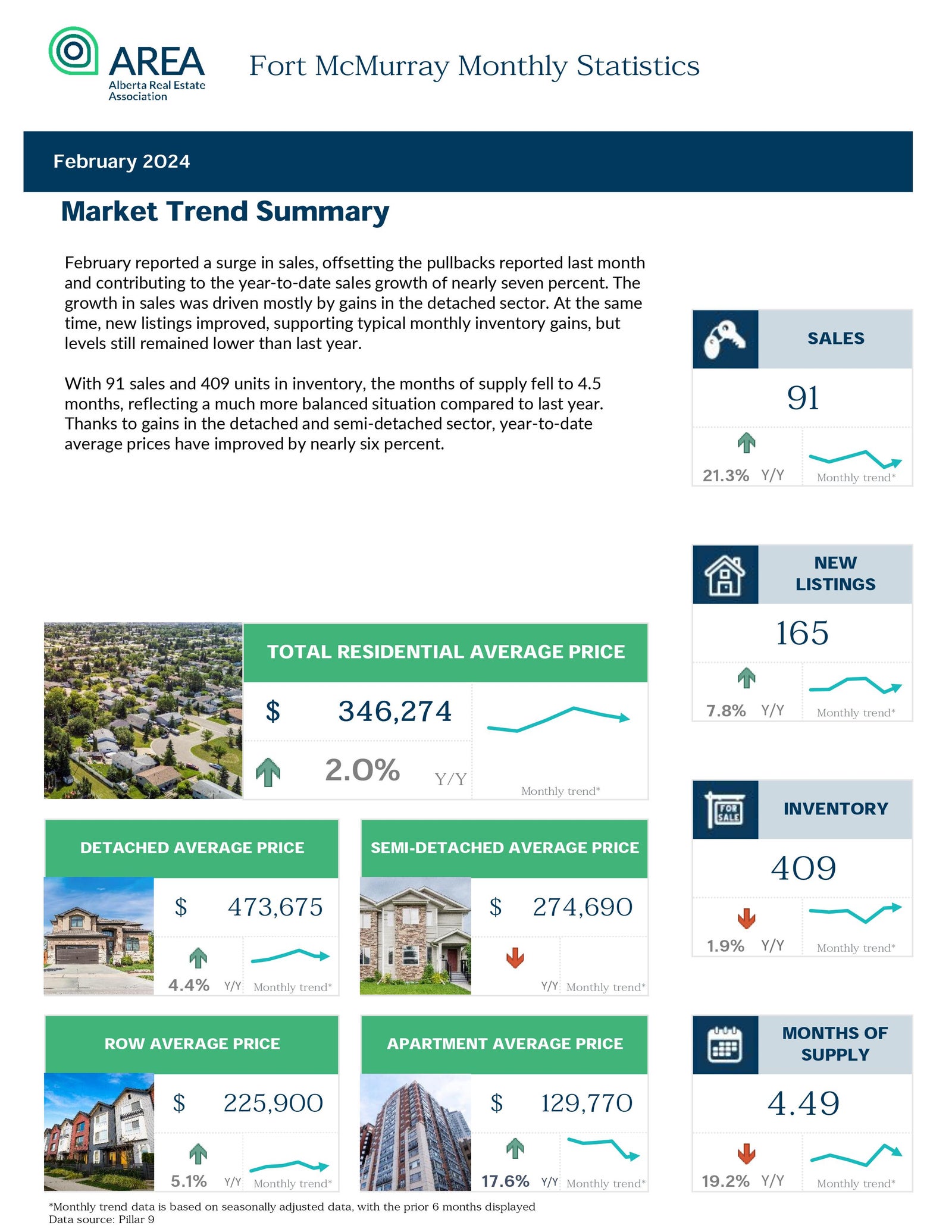

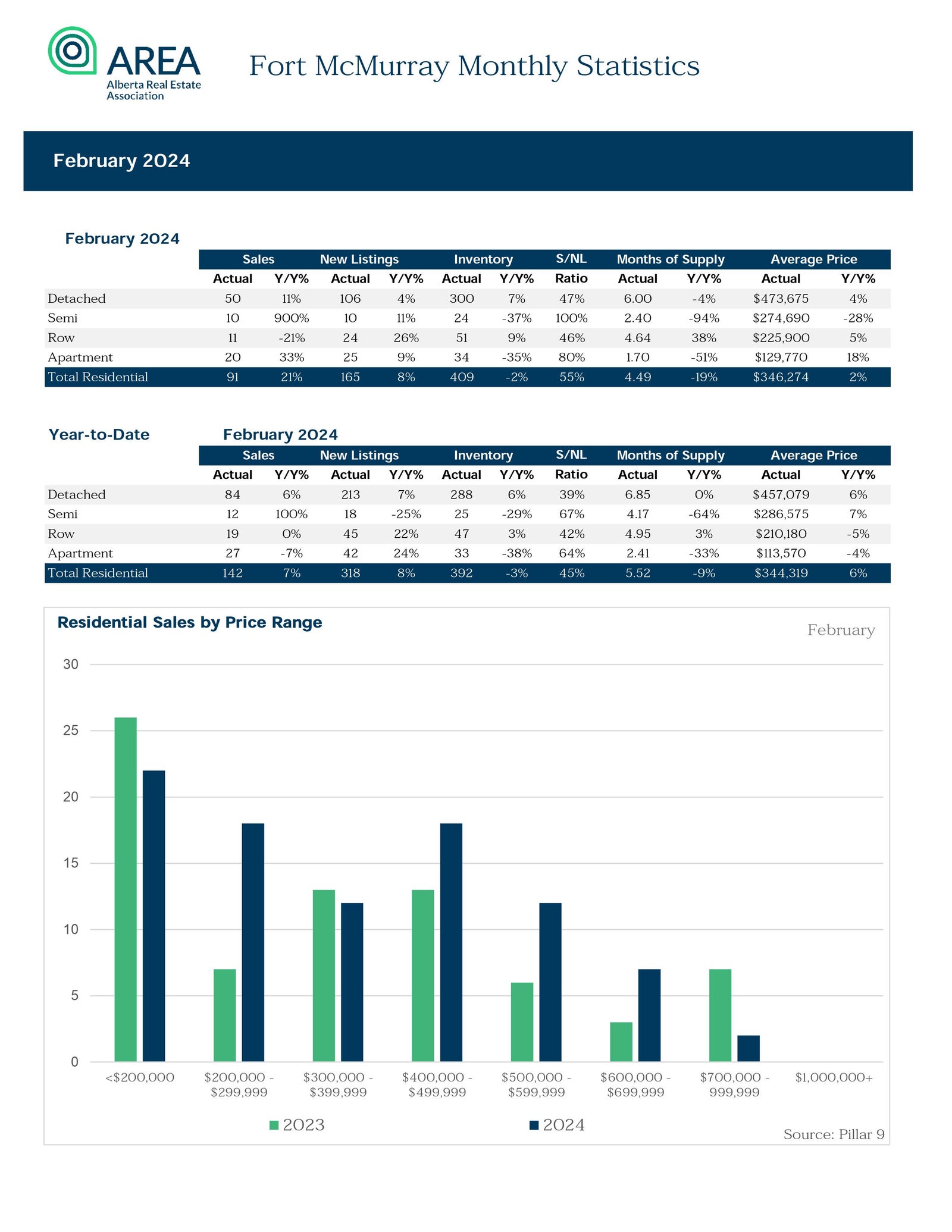

Housing Stats for February 2024

Posted on Mar 07, 2024

We had a surge in sales during February (91) compared to January (51).

The months of supply fell to 4.49 in February from 7.35 in January. This means we are moving in the direction of a balanced market if sales and new listings will continue in the same manner.

I feel confidant that we are heading into a busy Spring Market!

Housing Stats for October 2022

Posted on Nov 24, 2022

"October sales eased to the lowest levels reported for the month since 2017 as higher lending rates and a weaker employment market in the area continue to weigh on demand. However, recent pullbacks in sales have not entirely erased early gains in sales, as year-to-date sales remained comparable to last years levels. Nonetheless recent pullbacks in...

Housing Stats for May 2022

Posted on Jun 15, 2022

Sales activity during May 2022 (134) were lower than in April 2022 (157) but there is an increase in the year-to-date sales. The decrease in the detached homes prices May 2022 ($499,576) compared to April 2022 ($524,090) is a result of the decline in prices in the mobile homes section.

Let us stay positive - at least we are better off than a couple...

Let us stay positive - at least we are better off than a couple...

Housing Stats for April 2022

Posted on Jun 15, 2022

Thanks to another month of improving sales, year-to-date sales totaled

516 units a 20 percent rise over last year's levels and the strongest start

of the year since 2014. The growth was somewhat possible thanks to

the gain in new listings. However, it was not enough to have created any

significant shift in inventory levels.

With 359 units in inventory i...

Housing Stats for March 2022

Posted on Apr 15, 2022

"Sales activity increased in March, contributing to the best first-quarter start of the year since 2014. Some of the sales growth was only possible due to the rise in new listings. Monthly new listings have generally been trending up since the end of 2021, however, the growth in new listings was not enough to cause any substantial change in invento...

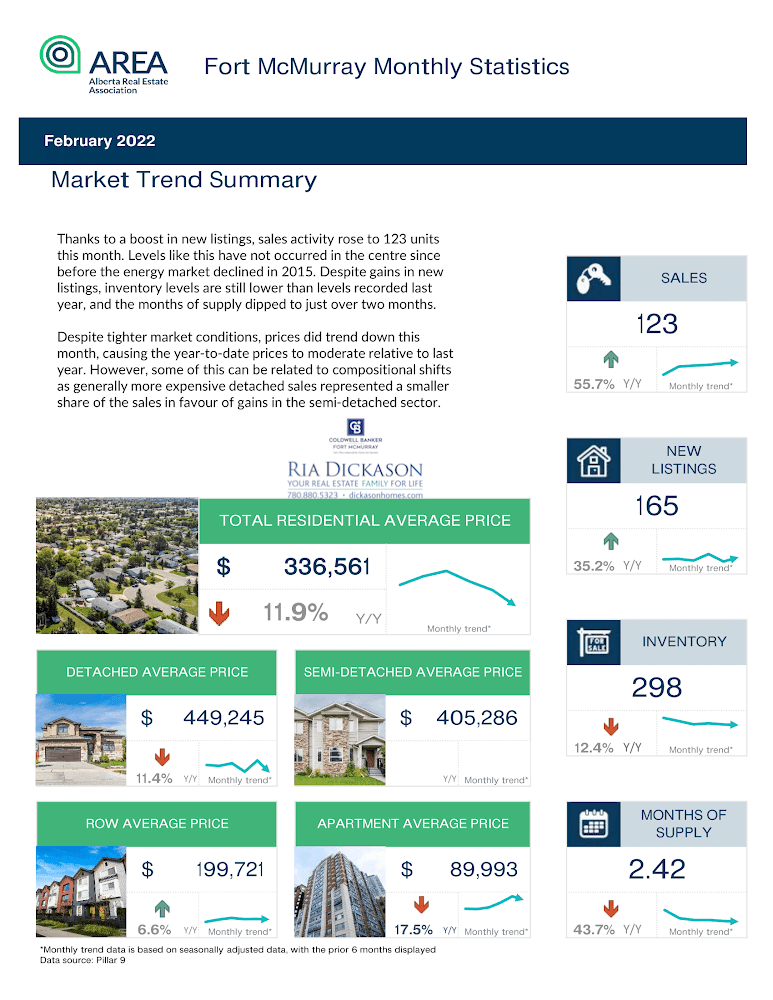

Housing Stats for February 2022

Posted on Mar 09, 2022

The market is busy and we have a Seller's market at the moment. We currently have only 2.42 months of supply.